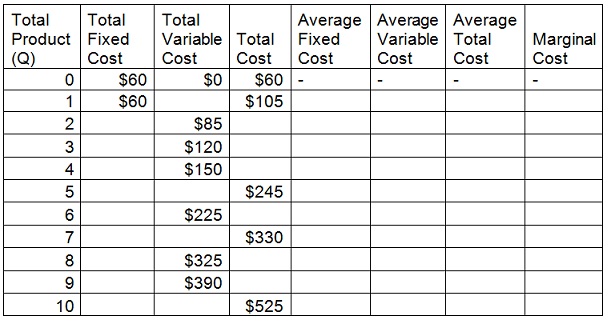

problem: Cost

a) Complete the given table:

b) Draw one graph of ATC, AVC and MC. Draw other graph with TC.

c) What happens to ATC as Q increases?

d) Where does MC cross AVC? ATC?

e) Assume that fixed costs increase by $20. How will this influence TFC, TVC, TC, ATC, AVC and MC? Which numbers change and which stay similar?

f) Assume that raw material prices increase by 20%. How will this influence TFC, TVC, TC, ATC, AVC and MC?

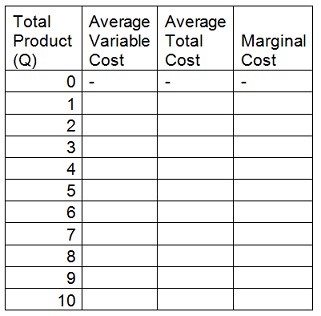

problem: Perfect Competition

a) What does it signify for a market to be perfectly competitive? What are the three conditions of perfect competition? What does it signify for firms to be ‘price takers’?

b) Let’s focus on just the per unit information from the table in problem #1. Complete the table.

c) Assume that the market price of this product is $57. How much would a profit maximizing firm choose to produce? Compute profits or losses.

Please note there are two ways to find the right answer to these problems. The tough way is to compute total revenue, total cost and profit for each possible quantity and then pick the Q that yields the maximum profit.

The simple way is to use marginal analysis. As I’m going to ask you to do this several more times with different prices, I propose you figure out the simple way.

d) How high does the price require being for firms to be able to make a profit? This is the long run shutdown price – if a firm can’t make a profit it will shutdown at certain point.

e) How low can the price go before a firm will shut down instantly?

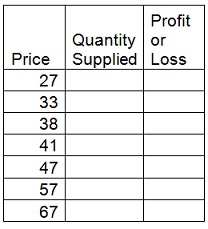

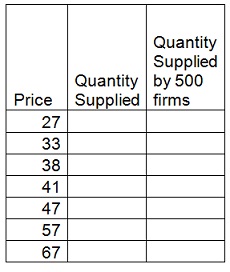

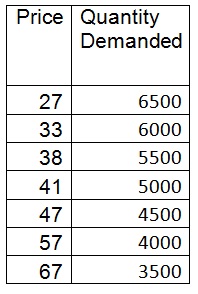

f) Now let’s scale up from 1 firm to many firms. Assume that there are 500 identical firms competing in this industry. Complete the table (it is really a supply schedule).

g) Graph the industry supply curve with Q on the horizontal and P on the vertical.

h) Take the given data on demand and add up it to your graph. Find the equilibrium price in this market.

i) How are firms doing at the equilibrium price? Are they earning profits or losing money? Do you expect the number of firms to mount or drop in this industry?

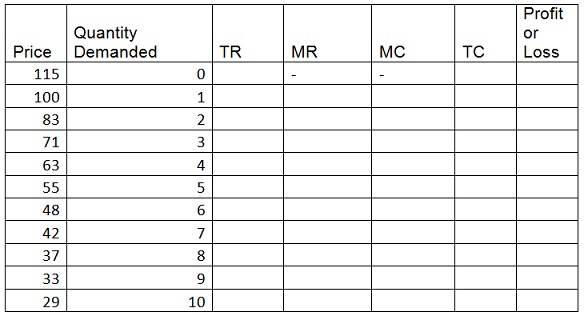

problem: Monopoly.

Use all the information on costs from problem #1, but now our firm has gained a monopoly and is the only seller for this product. Use the information in this table on demand, altogether with info on costs to answer the problems.

a) Complete the table.

b) Graph Demand, MC, and MR.

c) How much will a profit maximizing monopolist choose to produce? What price will they charge? Compute firm profits at this level of output.

d) What would happen if the monopolist produced one more unit? What would the cost of producing the next unit be? How much could the monopolist sell the next unit for? Why won’t the monopolist generate this next unit?

e) Is the monopoly outcome proficient? Are there some units that pass a cost benefit test which aren’t being produced? Show the dead-weight loss on your graph.